pdf. For effectuated registration entirely in the FFM, we omitted states with complete SBMs but included SBMs on the federal platform. For spending in the FFM states, we used the 2018 actual costs on health insurance coverage exchanges as reported in CMS budget documents. See "Justification of Price Quotes for Appropriations Committees, Centers for Medicare & Medicaid Providers, Department of Health & Human Solutions, Fiscal Year 2020, pp. 178-183 and 212, https://www. cms.gov/ About-CMS/Agency-Information/Performance, Budget/FY2020-CJ-Final. pdf. For spending by California's exchange, we used the 2018-2019 budget for Covered California, June 15, 2018, p. 26, https://hbex. coveredca.com/financial-reports/PDFs/Covered, CA_2018-19_Budget-6-15-18. pdf. For spending by Massachusetts' exchange, we utilized the Health Adapter Administrative Financing Update, slide discussion at the July 12, 2018 board of directors conference, p.

com/wp-content/uploads/ board_meetings/ 2018/07 -12 -18/ Health-Connector-Administrative-Finance-Update-VOTE-071218. pdf. For costs by Minnesota's exchange, we utilized the MNsure Three Year Plan, Financial Years 2019-2020-2021, gotten ready for the July 17, 2019 board conference, https://www. mnsure.org/assets/Bd-2019-07-17-DRAFT-FY20-budget_tcm34-393218. pdf. For spending by Washington's exchange, we used the Washington Health Benefit Exchange's financial report for the August 23, 2018 board conference, p. 4, https://www. wahbexchange.org/wp-content/uploads/2018/08/HBE_EB_180823_Finance-Update. pdf. States vary in how much they buy functions such as marketing and outreach to hard-to-reach populations and in how much they support small company registration. States also have different financing sources for their operations a crucial criterion for what its exchange might have available to spend. Vermont and New york city are presently the only states that restrict age-rating; in these states, plans charge the very same premium for grownups despite age. If you reside in one of these states, the Medical insurance Marketplace Calculator will determine your premiums according to your state's guidelines. Yes. The cost of medical insurance (your monthly premium) varies a fair bit by state, and even within regions of a state. This is because of a number of factors, such as the cost of living and expense of health care services in your location. Your premium tax credit is tied to the cost of insurance coverage in your location.

Premiums in the Health Insurance Coverage Market Calculator are real premiums in your location. It is possible that some plans might not be readily available in your particular zip code or county, though. For this reason, you may get somewhat various outcomes when you get subsidies through Healthcare. gov or your state's Marketplace. Yes, in many states, insurance companies can charge people who use tobacco a higher premium (this is called a "tobacco surcharge"). Currently, only Timeshare Cancellation Lawyer six states (California, Massachusetts, New Jersey, New York, Rhode Island, and Vermont) and the District of Columbia do not enable personal health strategies to charge higher premiums for individuals who utilize tobacco; and several other states limitation tobacco surcharges to less than 50%.

The health Are Timeshares Still A Thing law also makes clear that financial aid through the Medical insurance Market can not be utilized to cover the part of the premium that is due to a tobacco additional charge. The Health Insurance Marketplace Calculator does adjust your results based upon tobacco usage since tobacco surcharges vary rather a bit from strategy to strategy (How to get health insurance). Even in states that enable it, some insurance Jon Wesley Thompson providers select not to charge higher rates for tobacco users or charge fairly low additional charges. For this reason, the calculator warns you when you might deal with higher costs, however to learn your true expenses, you will require to go to Health care.

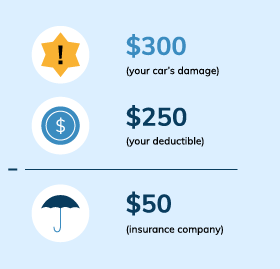

When you buy coverage through the Medical insurance Market you can select in between four levels of protection: Bronze, Silver, Gold, and Platinum. The levels are based on how much financial protection the strategies offer you when you get ill or need healthcare. Bronze plans will have the most affordable monthly premiums, but have the greatest deductibles, copayments, and other expense sharing. If you get ill or have an accident, your share of covered medical costs that you will have to pay out-of-pocket will be higher because of the higher expense sharing. What is an insurance premium. Silver strategies are more protective and will have higher regular monthly premiums, but normally have somewhat lower deductibles and other expense sharing, suggesting you would likely invest less out of pocket when you get treatment.

The Health Insurance coverage Marketplace Calculator reveals the cost of silver and bronze plans in your area. Silver plans are important because these are used as a "standard" for calculating how much help you are qualified for. The silver premium displayed in the calculator is the second-lowest-cost silver plan in your area. The Medical Insurance Market Calculator will likewise reveal you the price of the lowest-cost bronze strategy in your area. Bronze strategies are the most affordable level of coverage that many people are needed to have under the health law. If a Bronze plan is still unaffordable to you even after financial support, or if you are under the age of 30, you may acquire a devastating plan.

Getting The How Much Auto Insurance Do I Need To Work

Premium tax credits can not be applied to disastrous health insurance. For more details on the difference in between bronze and silver plans, see the question on actuarial worth, listed below. With many job-based health insurance, a company pays part of your regular monthly or yearly costs (premiums). In general, people who get approved for health insurance through their task are unable to get monetary assistance through the Marketplaces. However, if your company's protection is either unaffordable or does not fulfill the healthcare law's "minimum worth" requirement, then you may be eligible for monetary aid to acquire through the Market. "Minimum value" suggests your employer strategy pays a minimum of 60% of the total cost of medical services.